Running a barbershop with consistent bookings doesn't guarantee you'll make payroll next month. Too many shops close their doors while their appointment books stayed full, killed by cashflow gaps nobody saw coming.

The problem usually isn't that owners don't track money. It's that they track the wrong things at the wrong times. Revenue looks good this week, so everything feels fine. Then rent, supplies, and payroll all hit at once, and suddenly you're scrambling to cover a $4,000 gap with $900 in the account.

Most barbershops operate on what I'd call "checking account management"—if there's money in the account, we're good. That approach breaks down fast when you're juggling booth rent from independent contractors, retail inventory purchases, and seasonal swings that can cut revenue by 35% in slow months.

Why traditional budgeting fails barbershops

Standard small business budgeting assumes predictable monthly revenue. Barbershops don't have that. A strong Saturday can generate $3,500. A dead Tuesday might bring in $400. Your barbers take vacations, clients skip during holidays, and that new shop down the street just poached two of your regulars.

The typical barbershop cashflow cycle creates three specific pressure points that generic financial advice doesn't address:

Weekly payroll vs. monthly expenses: Your barbers expect their booth rent or commission checks weekly, but your major expenses hit monthly. This timing mismatch means you need roughly 40% of your monthly revenue sitting in reserve just to handle the overlap.

Retail inventory trap: Ordering product inventory requires upfront cash that won't convert back to revenue for 45-60 days. One aggressive product order can wipe out your operating cushion overnight.

Seasonal collapse periods: Most shops see revenue crater during specific windows—the week after Christmas, first week back to school, mid-July. A 50% revenue drop during these periods is normal. Without planning, it becomes a crisis.

The shops that survive these cycles don't just track money better. They build specific operational controls that prevent cashflow disasters before they start.

Building your minimum reserve calculation

Your minimum cash reserve isn't some arbitrary number. It's based on your actual weekly operating burn rate multiplied by your typical cashflow gap period.

Never miss a booking amidst the hustle.

Trimzly helps you schedule, confirm, and manage every client visit seamlessly.

- Unified appointment management

- Automated client reminders

- Optimized staff scheduling

No credit card required

Here's the formula that works for single-location barbershops:

Base calculation:

-

Weekly payroll/booth rent obligations

$_

-

Weekly operating expenses (averaged)

$_

-

Weekly loan/lease payments (if any)

$_

-

Total weekly burn rate

$_

Minimum reserve = Weekly burn rate × 3.5 weeks

Why 3.5 weeks? Because that covers the gap between your slowest revenue week and when monthly income typically recovers. For a shop with a $2,800 weekly burn rate, you need roughly $9,800 minimum in reserves at all times.

What most owners miss is that this reserve number changes with the season. During November-December, increase it by 25% to handle holiday volatility. During back-to-school season, bump it 15%.

The month-by-month tracking template

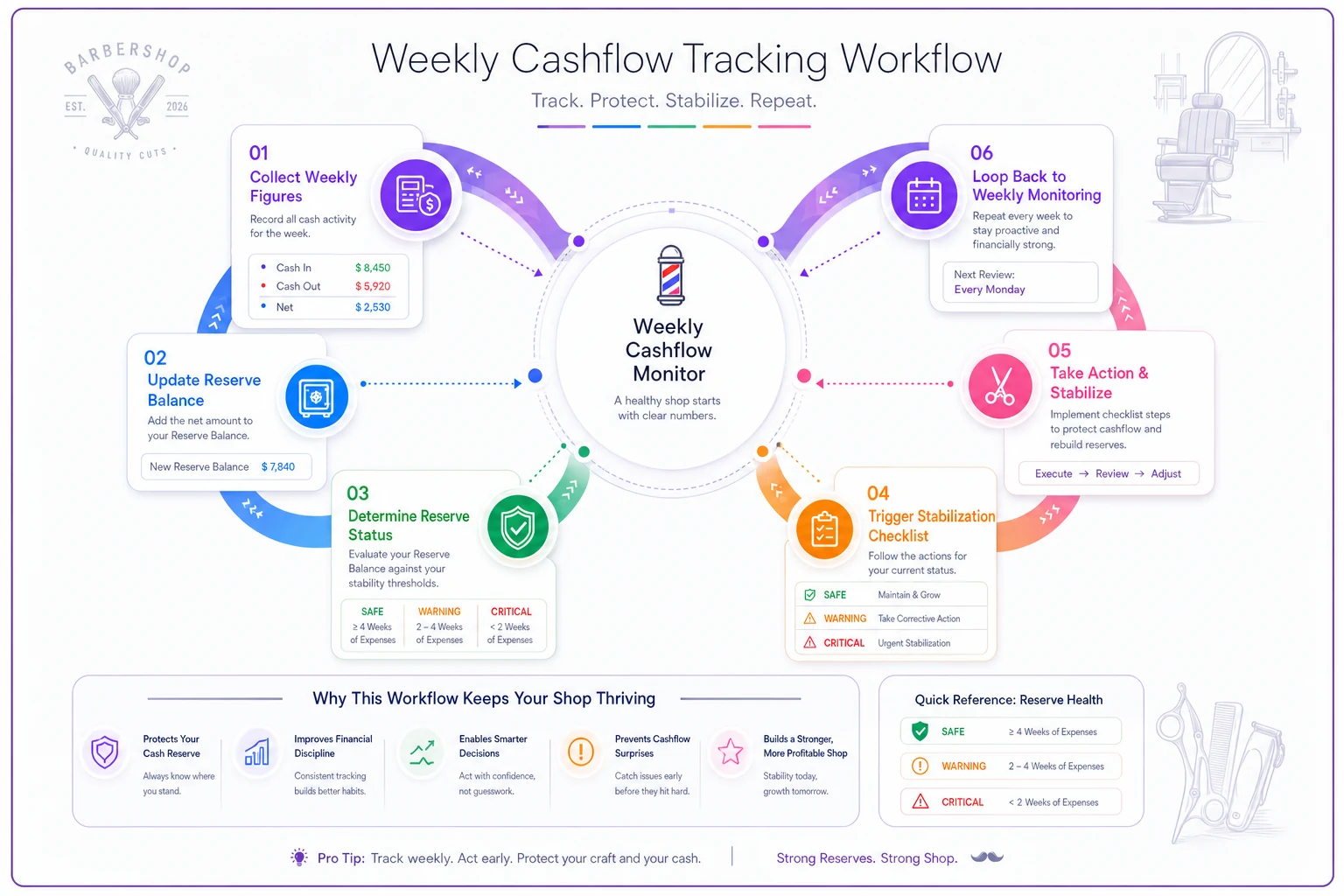

Forget complex spreadsheets with 47 tabs. Effective barbershop cashflow tracking needs just five numbers tracked weekly:

| Week Ending | Cash In | Cash Out | Net | Reserve Balance | Reserve Status |

|---|---|---|---|---|---|

| Week 1 | $4,200 | $3,100 | +$1,100 | $10,900 | Safe |

| Week 2 | $3,400 | $2,900 | +$500 | $11,400 | Safe |

| Week 3 | $2,100 | $3,200 | -$1,100 | $10,300 | Safe |

| Week 4 | $3,800 | $4,500 | -$700 | $9,600 | WARNING |

The "Reserve Status" column uses simple triggers:

-

Safe

Above minimum reserve

-

Warning

Within 10% of minimum

-

Critical

Below minimum

Track this weekly, not monthly. Monthly averages hide the danger zones. When you hit "Warning" status, specific protocols kick in—that's where your stabilization checklist comes in.

Here's a quick workflow for weekly tracking and reserve decision points.

Use this workflow to keep reserves visible and act on Warning status quickly.

Your 30/60/90 day stabilization checklist

When cashflow drops below safe levels, you need predetermined actions, not panic decisions. This isn't about slashing everything—it's about strategic adjustments that protect operations while rebuilding reserves.

30-Day Actions (Warning Status)

Start these immediately when reserves drop within 10% of minimum:

Immediate revenue adjustments:

-

Implement "same-week only" retail discounts (15% off for purchases made within current week)

-

Push gift card sales with small bonus ($5 extra value on $50 cards)

-

Contact top 20 clients for pre-booking next month's appointments

-

Run chair rental special for any empty stations (first month 25% off)

Controlled spending freeze:

-

Pause all non-essential supply orders

-

Delay any equipment upgrades

-

Switch to minimum retail reorder quantities

-

Hold on hiring or training expenses

Collection acceleration:

-

Call any outstanding booth rent, even if just 2 days late

-

Collect on any house accounts immediately

-

Cash out gift card liabilities where possible

These actions typically recover 10-15% of reserve within 30 days without damaging operations.

60-Day Actions (Sustained Warning)

If reserves don't recover within 30 days, escalate:

Service menu optimization:

-

Add express services at premium prices (15-minute beard trim at 80% of full service price)

-

Bundle slow-moving retail into service packages

-

Eliminate lowest-margin services temporarily

-

Push higher-ticket services through targeted booking incentives

Staffing adjustments:

-

Reduce overlapping coverage hours

-

Renegotiate booth rental terms (move to higher commission, lower fixed rent)

-

Cross-train staff to reduce coverage needs

-

Adjust operating hours based on actual traffic data

Vendor negotiations:

-

Request 15-30 day payment extensions from suppliers

-

Negotiate partial payments on larger bills

-

Switch to COD terms for better pricing

-

Consolidate orders to fewer vendors for volume discounts

90-Day Actions (Critical Status)

At 90 days without recovery, structural changes become necessary:

Revenue model shifts:

-

Convert booth renters to commission to reduce fixed costs

-

Sublease unused space or hours

-

Partner with complementary services (massage, nails) for space sharing

-

Launch membership programs for guaranteed monthly revenue

Deep cost restructuring:

-

Renegotiate lease terms or consider relocation

-

Eliminate all non-performing services and retail

-

Reduce hours to profitable periods only

-

Consider temporary closure of slow days

Emergency funding:

-

Open business line of credit while finances still qualify

-

Explore equipment refinancing

-

Investigate SBA emergency loans

-

Consider bringing in an operating partner or investor

Most shops recover at the 60-day mark if they actually follow the checklist. The 90-day actions are insurance—better to have the plan than to scramble when things get critical.

KPI triggers for automatic cost reduction

Don't wait for a gut feeling to trigger cost controls. Use specific KPI thresholds that automatically activate spending adjustments. This removes emotion from financial decisions.

Primary triggers:

Service utilization below 65%: When less than 65% of available appointments book, immediately pause any marketing spend for new clients and focus entirely on retention and rebooking.

Retail turn below 4x annually: If retail products aren't selling through at least four times per year, stop reordering and liquidate existing inventory at cost.

Barber productivity under $400/day: When any barber averages below $400 in daily services, restructure their compensation or hours before it drags down overall margins.

Walk-in percentage exceeds 30%: High walk-in rates usually mean scheduling inefficiency. When walk-ins exceed 30% of revenue, implement strict appointment-only hours during peak times.

Average ticket drops 10%: A sudden ticket drop signals discounting or service mix problems. Freeze all discounts and audit service times immediately.

Each trigger should have a specific response protocol. When service utilization drops below 65%, for example:

-

Audit last 30 days of no-shows and late cancels

-

Contact all clients who haven't booked in 45+ days

-

Reduce operating hours to consolidate appointments

-

Implement minimum service requirements for peak hours

These triggers catch problems while they're still manageable—usually 30-45 days before they'd show up in monthly financial statements.

Payroll contingency plans that protect your team

Payroll is sacred in barbershops. Miss one check and you'll lose good barbers, probably permanently. But when cash gets tight, you need predetermined plans that keep everyone paid while reducing costs.

Commission structure flexibility: Build commission agreements with automatic adjustments based on shop performance. When monthly revenue drops below certain thresholds, rates adjust temporarily. This shares the burden without anyone going unpaid.

For example:

-

Normal month (above $25K revenue)

60% commission

-

Warning month ($20-25K revenue)

55% commission

-

Critical month (below $20K revenue)

50% commission

Barbers agree to this upfront, understanding it protects everyone's long-term stability.

Booth rent deferrals: For booth renters, offer partial payment options during critical periods. Instead of demanding full $300 weekly rent when cash is tight, accept $200 now and $100 deferred to the following month when things recover. This keeps chairs filled while managing immediate cash needs.

Owner salary flexibility: Your pay comes last and should be the most flexible line item. Build your personal finances to handle 60-90 days without drawing from the business. When reserves hit warning levels, stop owner draws immediately.

Cross-coverage agreements: Partner with nearby shops for emergency coverage arrangements. If you need to temporarily reduce hours or staff, having placement options for your barbers maintains relationships for when things recover.

Real scenario: How one shop used this system

A barbershop in suburban Atlanta implemented this exact cashflow system after nearly missing payroll twice in six months. Six chairs, mixed booth rental and commission, averaging $28K monthly revenue.

Their weekly burn rate calculated to $3,400, setting their minimum reserve at $11,900. Within two weeks of tracking, they discovered they were operating with only $4,000 in reserves—basically one bad week from crisis.

Using the 30-day stabilization checklist, they:

-

Ran a gift card promotion that brought in $2,200 immediate cash

-

Negotiated payment terms with their retail supplier, freeing up $1,800

-

Reduced overlapping coverage, saving $400 weekly

By day 45, reserves had rebuilt to $9,500. They stayed in warning status for another month but never hit critical. Six months later, they maintained steady reserves around $14,000 and hadn't faced another cashflow scare.

The key wasn't complex financial management—it was having clear triggers and predetermined actions that kicked in when specific thresholds were crossed.

Technology and cashflow management

Modern operational software can automate a lot of this tracking and trigger system. Instead of manually calculating weekly burn rates and reserve levels, AI-powered platforms can pull data directly from your booking system, POS, and payment processing to maintain real-time cashflow visibility.

These systems particularly help with:

-

Automatic alert generation when KPIs hit trigger points

-

Predictive cashflow modeling based on booking patterns

-

Integration between scheduling and financial tracking

-

Automated reporting that shows exactly where cash is going

The automation matters because cashflow management fails when it requires daily manual work. Shop owners get busy, skip a week of tracking, and suddenly they're in crisis mode. When the tracking happens automatically and alerts push to your phone, problems get caught while they're still solvable.

Some platforms can also analyze booking patterns and suggest specific schedule optimizations that improve cash position—identifying that moving one barber's schedule by two hours could increase weekly revenue by a few hundred dollars by better matching availability to demand.

Making this system stick

The hardest part isn't building the system—it's maintaining it when things get busy. Successful implementation needs three things:

Weekly review rhythm: Pick a specific day and time for your weekly cash position review. Tuesday mornings work well because you have Monday to collect weekend data but still have time to implement adjustments before the week gets away from you.

Triggered responses, not judgment calls: When a KPI hits its trigger point, execute the predetermined response immediately. Don't wait to "see how next week goes." The whole point of triggers is removing emotion and delay from financial decisions.

Team transparency: Share appropriate cashflow information with your team. When barbers understand the shop's financial position, they're more likely to support necessary adjustments. You don't need to share everything—basic health indicators are enough to help everyone row in the same direction.

Put your weekly cash review on a shared calendar invite and set a reminder 30 minutes before—consistency prevents skipped checks.

Your barbershop operating system needs financial controls just as much as it needs service standards. And just like ramping new barbers, managing cashflow requires structured checkpoints and clear success metrics.

Most barbershops fail not because they can't attract clients or deliver great cuts—they fail because they run out of cash during predictable rough patches. This checklist turns those predictable problems into manageable situations with clear solutions.

Start with calculating your real weekly burn rate. That single number tells you more about your shop's financial health than any monthly P&L statement. From there, build your reserves, implement your triggers, and watch your financial stability improve week by week.

Ready to elevate your barbershop operations?

Join 500+ barbershops using Trimzly to save time, reduce scheduling conflicts, and enhance client satisfaction.